Pool insurance isn’t a separate policy — it’s a piece of your homeowner’s insurance that most DFW pool owners don’t fully understand until something breaks and they’re staring at a repair bill wondering if they can file a claim. Here’s the reality: your homeowner’s policy does cover some pool damage, but far less than most people assume. The difference between a claim that gets paid and one that gets denied often comes down to one word — “sudden.” If you’ve ever asked “does homeowner’s insurance cover pool damage?” the honest answer is: it depends, and getting it wrong costs thousands.

This guide covers exactly what your pool insurance covers, what it doesn’t, how to file a pool damage insurance claim properly, and how professional maintenance actually strengthens your position with the insurance company.

The Short Answer on Pool Insurance — It Depends, and Most Owners Get It Wrong

The key distinction in every pool insurance question is sudden and accidental damage versus gradual deterioration and maintenance failure. Your homeowner’s policy is designed to cover events that happen unexpectedly — a tree falling on your equipment during a storm, a lightning strike frying your control board, someone vandalizing your pool.

What it’s NOT designed to cover is stuff that happens slowly over time because you didn’t maintain things — a pump motor burning out after 12 years, plaster deteriorating, a slow leak getting worse over months. According to the Insurance Information Institute, understanding this distinction before something happens saves pool owners from expensive surprises when they try to file a claim.

What Your Pool Insurance Typically Covers in Texas

Storm Damage

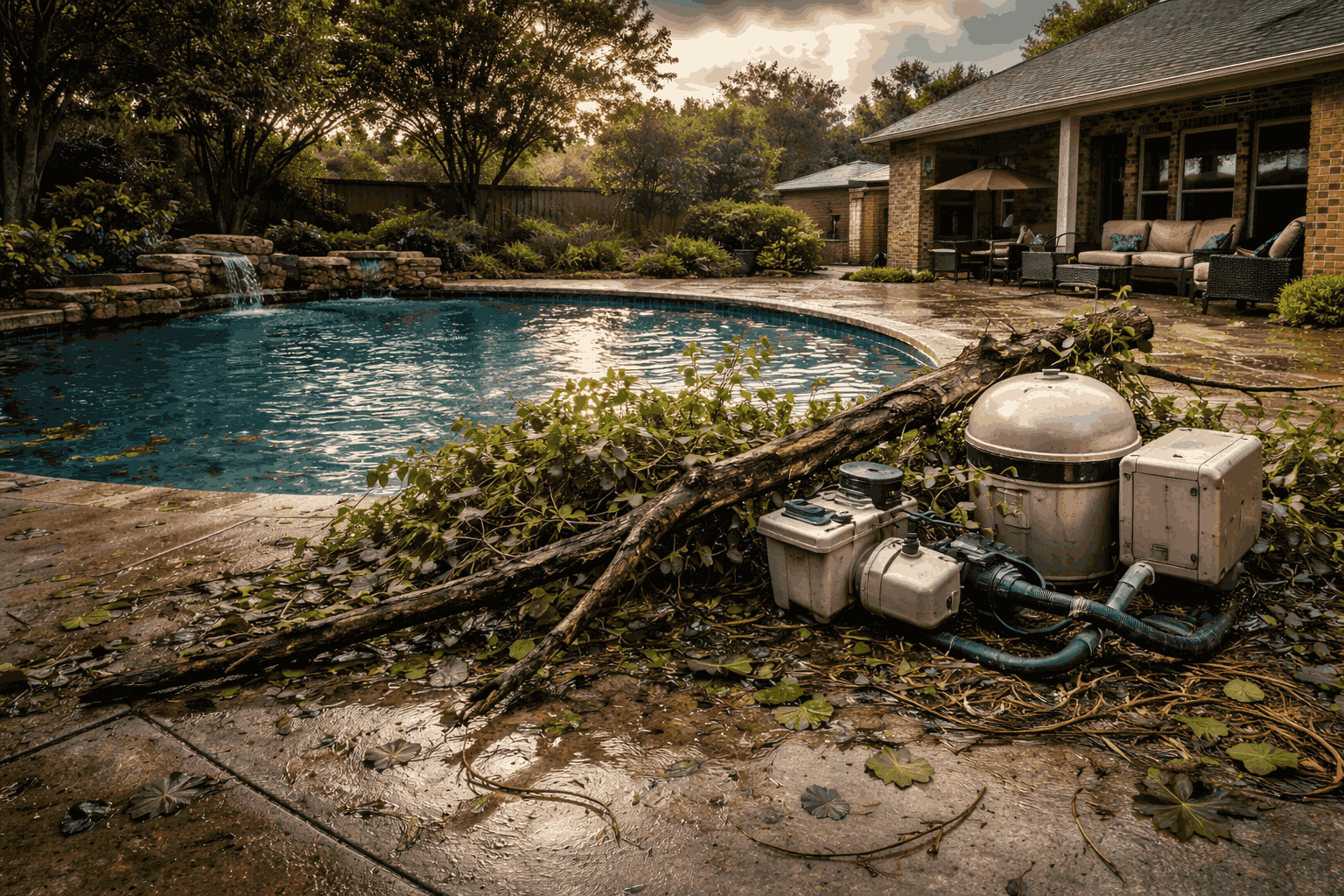

This is the most common covered pool damage insurance claim in DFW. A tree branch crashes into your pump during a thunderstorm — covered. Hail damages your equipment enclosure — covered. Wind blows debris that cracks your filter housing — covered. Lightning strikes and fries your automation control board, pump motor, or salt system — covered. North Texas storm season generates a lot of legitimate pool insurance claims, and these are the ones that typically get paid without much hassle.

Fire and Vandalism

Equipment damage from a nearby fire, deck and structural damage from fire, and intentional vandalism to your pool property are all standard covered perils under most Texas homeowner’s policies. Theft of equipment is rare but also covered. These types of pool damage insurance claim situations are straightforward since the cause is clearly sudden and not maintenance-related.

Certain Sudden Accidents

A vehicle driving into your pool area, a sudden pipe burst (not a gradual leak), and structural collapse from a covered peril are all typically covered. The word “sudden” is doing the heavy lifting here — if the damage happened quickly and unexpectedly, your pool insurance is far more likely to pay the claim.

Liability — Often the Most Valuable Pool Insurance Coverage

If someone gets injured in or around your pool — a slip-and-fall, a diving accident, or worse — your homeowner’s liability coverage handles medical payments and legal defense. This is often the most financially significant pool insurance coverage you carry, and the Consumer Product Safety Commission reports that pool-related injuries result in thousands of emergency room visits annually. Proper pool safety measures reduce this risk dramatically, and they also demonstrate responsible ownership to your insurer.

What Pool Insurance Typically Does NOT Cover — The Gaps That Cost Thousands

Normal Wear and Tear

Your pool pump dying after 10 years of service? Not covered. Plaster deteriorating with age? Not covered. Tile cracking from decades of thermal cycling? Not covered. Equipment reaching end of life and failing under normal use is considered maintenance, not an insurable event. This is the gap that surprises most DFW pool owners when they try to file a pool damage insurance claim for equipment that simply wore out.

Maintenance-Related Damage

Algae damage because you neglected maintenance for months — not covered. Chemical damage to surfaces from improper treatment — not covered. Equipment failure because you never serviced it — not covered. Insurance companies look at maintenance history when evaluating claims, and neglect is a legitimate reason to deny a pool damage insurance claim. This is where documented professional maintenance becomes incredibly valuable.

Gradual Leaks and Seepage

Slow plumbing leaks that develop over time are almost never covered. Underground pipe deterioration, soil erosion from long-term water loss, and gradual seepage through pool walls fall under the “gradual” category that pool insurance excludes. A sudden pipe burst is covered. A pipe that’s been leaking slowly for six months is not. That distinction matters enormously.

Freeze Damage — The Big One for North Texas Pool Insurance

This is where it gets complicated for DFW pool owners, and it’s the most contested type of pool damage insurance claim in our market. Some policies cover sudden freeze damage to plumbing and equipment. But many policies include language requiring you to have taken “reasonable precautions” to prevent freeze damage. If you didn’t winterize, didn’t run the pump during the freeze, didn’t drain exposed equipment — your claim may be denied.

The Texas Department of Insurance recommends reviewing your specific policy language before freeze season arrives. Policy language varies dramatically between carriers, and the time to understand your coverage is BEFORE a freeze event, not after. Having professional freeze protection documentation from your pool service creates evidence that you took those “reasonable precautions.”

Flood Damage

Standard homeowner’s insurance does NOT cover flood damage. If your pool area floods from rising water — not a pipe burst, but actual flooding — it’s not covered under your regular policy. The National Flood Insurance Program through FEMA offers separate flood insurance that may cover some pool-area damage, but coverage specifics vary. DFW homeowners in flood-prone areas should check whether their pool insurance gap includes flood exposure.

Settling and Ground Movement

Pool deck cracks from soil expansion and contraction, pool structure shifting from ground movement, and related damage from DFW’s expansive clay soil are NOT covered. This is a major gap for North Texas homeowners specifically, because soil movement is one of the most common causes of pool damage in our market. Earth movement exclusions are standard in Texas homeowner’s policies.

Cosmetic Damage

Staining, discoloration, surface roughness, and fading from UV exposure are all considered cosmetic and fall outside what pool insurance covers. Even if a stain makes your pool look terrible, it’s not an insurable loss unless it resulted from a covered peril like a chemical accident or equipment malfunction.

How to File a Pool Damage Insurance Claim in Texas

If you do have a legitimate pool damage insurance claim, here’s the process.

Step 1: Document everything immediately — photos, videos, dates, and a written description of what happened. The more evidence you capture right away, the stronger your claim.

Step 2: Take steps to prevent further damage. Temporary repairs to stop water loss or secure damaged equipment are usually reimbursable.

Step 3: Contact your insurance company promptly — most policies have time limits for reporting damage.

Step 4: Get a professional assessment and written repair estimate from your pool service provider.

Step 5: Keep every receipt and record related to the damage and any temporary repairs.

Step 6: Be prepared for the adjuster’s visit — they’ll want to inspect the damage firsthand.

One thing many homeowners don’t realize: many pool damage claims fall below the deductible threshold. If your deductible is $2,500 and the repair costs $2,000, there’s no point filing. Know your deductible before you start the claims process.

How Professional Pool Maintenance Strengthens Your Pool Insurance Position

This is where pool insurance and professional pool service intersect in a way that saves homeowners real money. Documented maintenance history proves “reasonable care” — the standard insurance companies use when evaluating claims. Service records demonstrate you didn’t neglect the pool, which removes one of the most common grounds for claim denial. Professional winterization records specifically support freeze damage claims by showing you took preventive action.

Regular equipment inspections documented in service reports show proactive maintenance that an adjuster can verify. According to the Insurance Information Institute, maintaining your property is one of the best ways to ensure claims aren’t denied for negligence.

PoolBurg provides digital service reports at every visit that create exactly this kind of documentation trail. Every chemical test, every equipment check, every issue flagged — it’s all recorded and available if you ever need to prove to an insurance company that your pool was professionally maintained.

People Also Ask

Does homeowner’s insurance cover pool equipment failure?

Only if the failure was caused by a covered peril like a lightning strike, storm damage, or power surge. Normal equipment failure from age or wear is not covered by pool insurance. A pump motor dying at 10 years old is maintenance, not an insurable event.

Is pool freeze damage covered by insurance in Texas?

It depends heavily on your specific policy language. Many Texas policies cover sudden freeze damage but require evidence that you took “reasonable precautions” to prevent it. Professional winterization documentation from your pool service is the strongest evidence you can have. Review your policy before freeze season — not after a pool damage insurance claim gets denied.

Does insurance cover pool resurfacing?

Not for normal deterioration. Pool resurfacing due to age, chemical wear, or UV exposure is considered maintenance. If the surface was damaged by a covered peril — like a falling tree cracking the plaster — the repair may be covered. But routine replastering is on you.

What should I do if a tree falls on my pool equipment?

Document the damage immediately with photos and video. Prevent further damage by shutting off power to the affected equipment. Contact your insurance company within 24 hours. Then call your pool service for a professional damage assessment and repair estimate. Storm damage from falling trees is one of the most commonly covered pool damage insurance claim types in DFW.

Does having a pool increase my homeowner’s insurance?

Usually yes, modestly. The National Association of Insurance Commissioners notes that pools increase liability exposure, which can raise premiums. Most Texas homeowners see a $50 to $100 annual increase. Having proper pool safety features like fencing, alarms, and drain covers can offset some of that increase.

Can my insurance claim be denied if I didn’t maintain my pool?

Yes. Insurers can and do deny claims when they determine the damage resulted from neglect rather than a covered peril. This is why documented professional pool insurance protection through regular maintenance records is so valuable. Proving reasonable care is your best defense against a denial.

PoolBurg — Your Maintenance Records Are Your Pool Insurance Backup

At PoolBurg, every service visit generates a digital record — chemistry readings, equipment condition notes, issues flagged, actions taken. That documentation trail isn’t just good pool management. It’s your strongest asset if you ever need to file a pool damage insurance claim. We also provide professional winterization services that create exactly the kind of “reasonable precautions” evidence Texas insurers look for when evaluating freeze damage claims. Your pool insurance only works as well as your ability to prove you held up your end of the deal — and that’s exactly what our service records do across all 17 DFW cities we serve.

Protect your investment and your insurance standing — professional maintenance by PoolBurg creates the documentation trail you need.